Win the Week™ Retail Newsletter (Nov. 30, 2024)

Dear Reader,

Welcome to our latest edition of the Win the Week newsletter, covering consumer spending trends for the week ending November 30, 2024.

We're excited to announce that we've expanded our coverage to include the Cosmetics category, featuring major beauty retailers like Sephora and Ulta Beauty. This addition comes at a perfect time as this week's data captures Black Friday and the start of the holiday shopping season, showing dramatic increases across most retail categories.

Let's dive into the numbers and analyze the most recent retail spending trends and consumer shopping behaviors.

The latest highlights are featured below.

General Retail Spending

Skyrocketing past last week’s spending increases, general retail spending this week increased substantially across the board, with extraordinary positive growth in both week-over-week (WoW) spend growth and average ticket growth (ATG).

Specifically, when compared to last week’s general retail spending data, every brand tracked experienced incredible upticks in ATG, with TEMU and Walmart ATG up 4.2% and 5.6%, respectively, putting them on the low end, while Target and Amazon saw much larger increases of 12.3% and 13.9%, respectively.

That generally carried over into WoW spend growth too, more moderate growth for TEMU and Walmart, up 2.2% and 13.3%, respectively, while Target and Amazon WoW growth, with Walmart up 31% and 30%, respectively.

Combining that data, here’s how general retail spending changed last week when compared to the previous 7-day period:

Weekly spend growth: 23.7%

Average ticket growth: 10.6%

Fast Fashion Spending

With a few declines this week, fast fashion spending had some slight growth in average ticket while weekly spend growth increased across the board.

For average ticket growth, SHEIN and H&M had negative growth, with ATG dropping by 1.3% and 2.8%, respectively. In contrast, Uniqlo and Zara had wild upticks in ATG, with average ticket growth for these brands rising by 0.9% and 2.3%, respectively.

With weekly spend growth, all brands saw positive growth this week, with SHEIN and Uniqlo at the low end, up 14.8% and 50.9%, respectively, while the big winners were Zara and H&M, with positive growth of 50.9% and 66.2%, respectively.

Overall, that meant that fast fashion spending last week had:

Weekly spend growth: 62.1%

Average ticket growth: 4.3%

Cosmetics Spending

As a new addition to this series, we’re now covering cosmetics as a stand-alone category that analyzes spending at Ulta and Sephora. This week started out with some positive and negative growth, with ATG for Ulta and Sephora down 1.1% and 4.7%, respectively, while WoW spend grow was up for both brands, increasing by ~106% and 67.7%, respectively.

Putting that data together, here’s how ATG and WoW spend growth changed for cosmetics spending last week:

Weekly spend growth: 86.7%

Average ticket growth: 5.6%

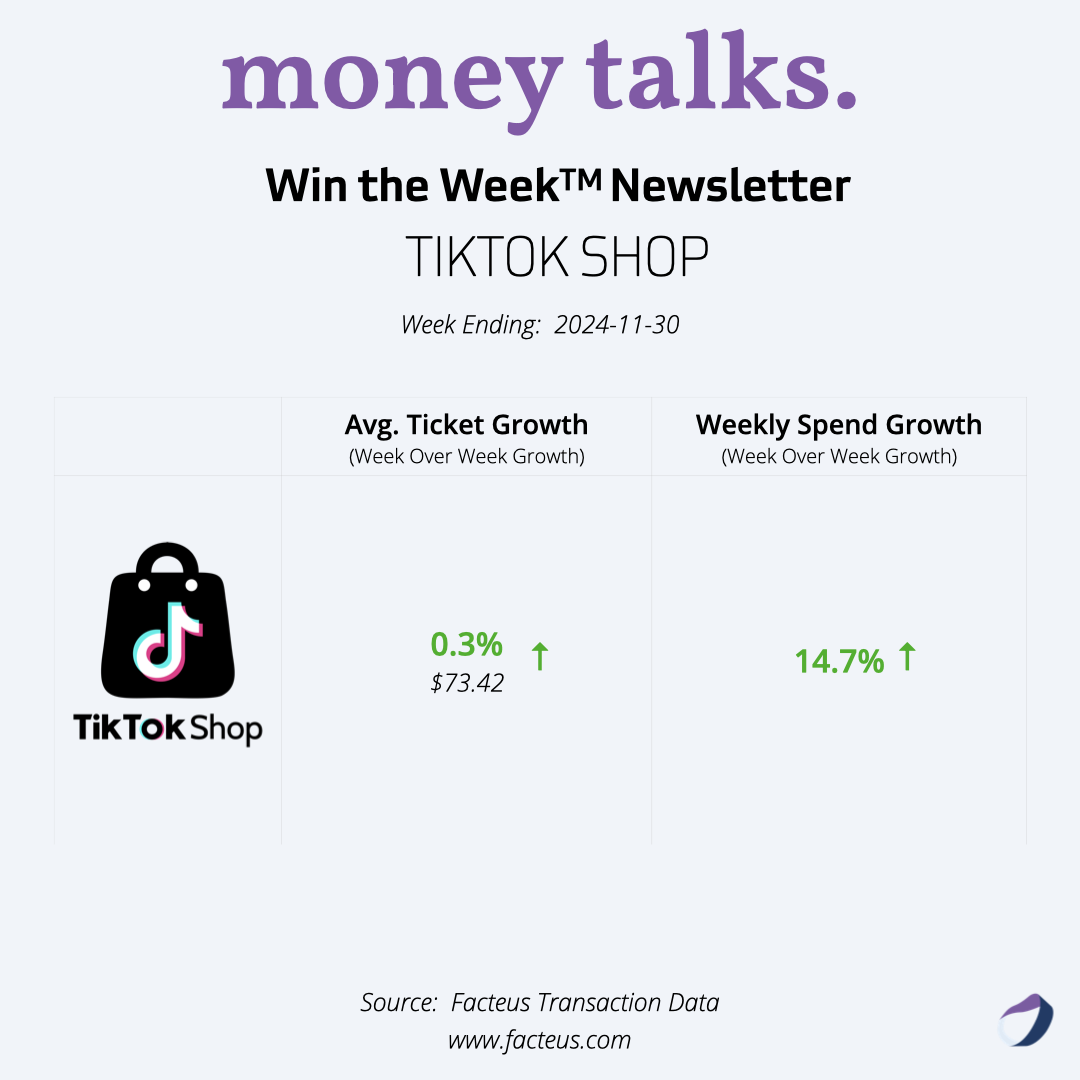

TikTok Shop Spending

Like general retail spending this week, spending on TikTok Shop spiked, with:

Weekly spend growth: 14.7%

Average ticket growth: 0.3%

This growth has kicked off a weeks-long trend of spikes in TikTok Shop spending, which could bode well for the rest of the holiday shopping season.

Other Retail Categories

Showing more declines this week when compared to any other category, retail spending in other categories was up for some — like Grocery Stores, Wholesale Clubs, and Hardware/Home Supply Stores — while it was down for others — like Fast Food, Restaurants, and Discount Stores. That is exactly what we saw last week too, starting a 2-week trend in these dips and upticks.

With ATG, Fast Food & Restaurants once again had the largest declines this week, dropping off 13.7%, while the average ticket growth at Discount Stores fell by 8.8%. Somewhat offsetting those dips were the upticks in ATG for Hardware/Home Supply Stores (up 4.5%), Wholesale Clubs (up 4.8%), and Grocery Stores (0.2%).

WoW spend growth brought slightly more growth, with only Fast Food & Restaurants dropping here, dipping by 3.1%. Here’s how weekly spend growth shifted across other retail categories this week:

Grocery spend growth: 5.7%

Wholesale Club spend growth: 1.8%

Discount Store spend growth: 26.2%

Hardware & Home Supply growth: 17.1%

Key Takeaways & Comparisons

Putting this week’s retail transaction data in context with recent consumer intelligence, new trends for several retail sectors begin to emerge, including for:

Black Friday Impact: The dramatic surge in spending is evident across almost all retail categories, with General Retail showing a robust 23.7% growth. Target and Amazon led the way with 31.0% and 30.0% growth respectively.

Fast Fashion Explosion: The apparel category saw remarkable growth of 62.1%, with individual retailers showing exceptional performance - H&M (70.9%), ZARA (66.2%), and UNIQLO (50.9%) all posted significant gains.

Cosmetics Surge: The beauty category demonstrated extraordinary growth, with Ulta Beauty leading at 106.0% growth and Sephora following at 67.7%, indicating strong holiday gift purchasing in this category.

Discount and Home Improvement: Discount stores showed strong performance at 26.2% growth, while Hardware & Home Supply increased by 17.1%, suggesting consumers are investing in both gifts and home preparations for the holiday season.

TikTok Shop: Maintained positive momentum with 14.7% growth, though not as dramatic as traditional retail channels during Black Friday.

The data this week presents a clear picture of robust Black Friday shopping activity across multiple retail categories.

The significant increases in average ticket sizes, particularly in General Retail (10.6%) and Cosmetics (5.6%), suggest that consumers are making larger purchases, likely taking advantage of holiday deals and promotions.

The exceptional performance in the Cosmetics category is particularly noteworthy, with both major beauty retailers showing triple-digit or near-triple-digit growth. This could indicate that beauty products are becoming an increasingly important category for holiday gift-giving.

The continued strength in Grocery (5.7%) and Wholesale Club (1.8%) spending suggests that consumers are maintaining their essential purchases while significantly increasing their discretionary spending for the holidays.

The modest decline in Fast Food & Restaurant spending (-3.1%) might indicate that consumers are prioritizing retail purchases over dining out during this major shopping period.

As we move deeper into the holiday shopping season, these strong Black Friday numbers suggest robust consumer confidence and willingness to spend. The broad-based nature of the growth across multiple retail categories indicates that holiday shopping is off to a strong start in 2024.

Remember, Facteus analyzes over $3.1 trillion in consumer spending from more than 120 million individual consumers, providing comprehensive insights across various industries.

If you have any questions or would like to explore how Facteus' data can support your business decisions, please don't hesitate to reach out.

Best regards,

Explore Our Win the Week™ Retail Spending Series