Win the Week™ Retail Newsletter (Dec. 7, 2024)

Dear Reader,

Welcome to our latest edition of the Win the Week newsletter, covering consumer spending trends for the week ending December 7, 2024. This week's data shows interesting shifts in spending patterns following the Black Friday/Cyber Monday period.

Let's dive into the numbers and analyze the most recent retail spending trends and consumer shopping behaviors.

The latest highlights are featured below.

General Retail Spending

Building on last week’s spending increases, general retail spending this week increased, with most big box retailers tracked experiencing positive growth in both week-over-week (WoW) spend growth and average ticket growth (ATG).

Specifically, when compared to last week, only TEMU has negative growth in ATG, with a slight dip of 1.2%, putting the average ticket at just over $67. In contrast, Amazon, Walmart, and Target had positive ATG of about 7.6%, 9.3%, and 10%, respectively.

Looking at WoW spend growth, all big box retailers tracked experienced positive growth last week, with Walmart, Target and TEMU at the lower end (0.1%,1.1%, and 2.0%, respectively) while Amazon was the “winner” in WoW growth, up 15.8% last week.

Combining that data, here’s how general retail spending fluctuated last week when compared to the previous 7-day period:

Weekly spend growth: 9.6%

Average ticket growth: 7.8%

Fast Fashion Spending

In contrast to general retail this week, fast fashion spending zigzagged around, with across-the-board declines in weekly spend growth while ATG had some gains for a couple of retailers.

In particular, average ticket growth was down for Zara and Uniqlo, dropping by 3.3% and 3.4%, respectively. SHEIN and H&M, on the other hand, recovered this week to experience positive ATG, with increases of 5.4% and 9.3%, respectively.

In terms of weekly spend growth, all brands had negative growth this week, as noted above, with SHEIN and Uniqlo at the low end, down 3.4% and 19.0%, respectively, while Zara and H&M had even deeper losses of 29.9% and 33.0%, respectively.

For the fast fashion spending last week, that data resulted in the following:

Weekly spend growth: -11.0%

Average ticket growth: 7.6%

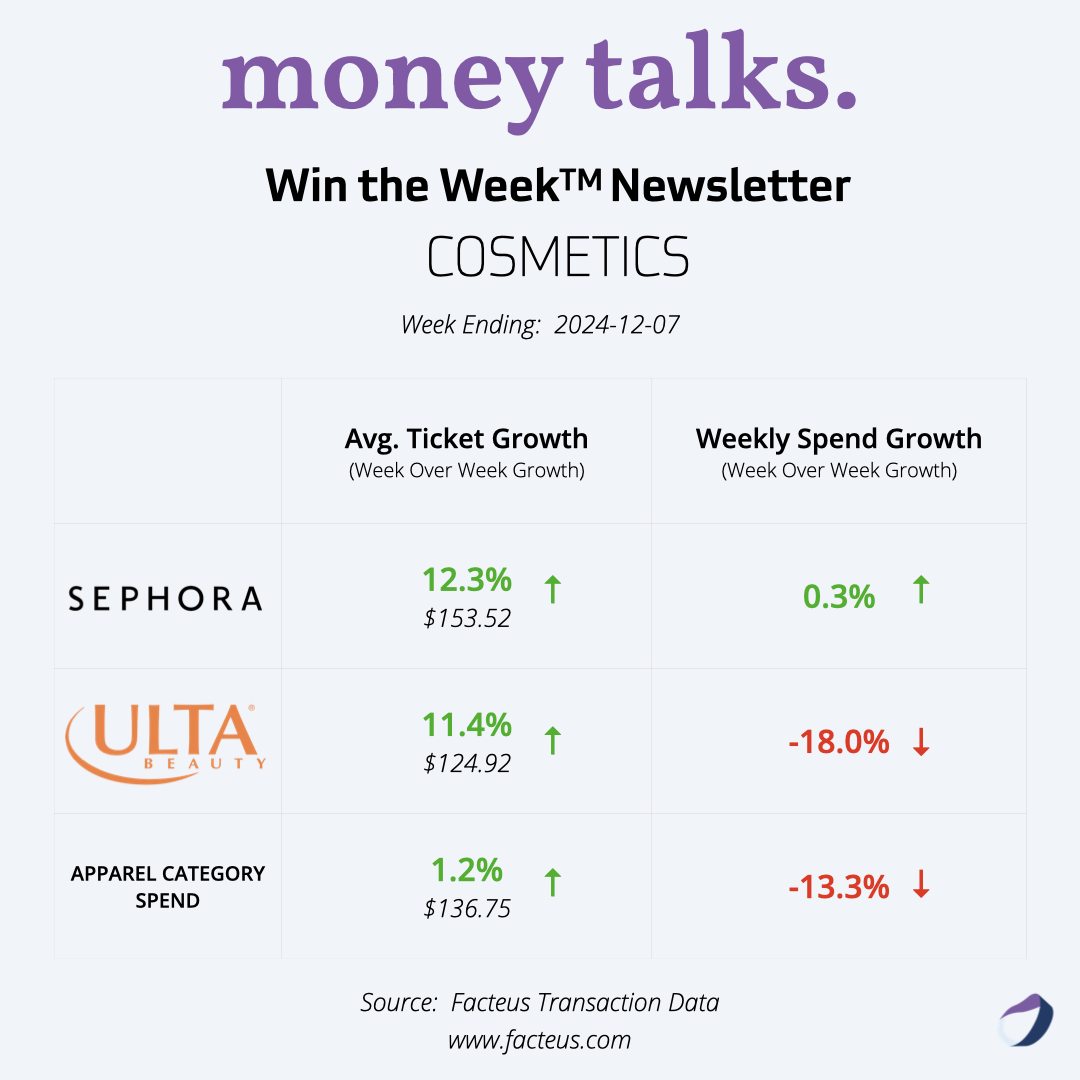

Cosmetics Spending

Also dropping off this week, cosmetics spending included a mix of positive and negative growth, with ATG for Ulta and Sephora up 11.4% and 12.3%, respectively, while WoW spend growth was more mixed, with Sephora up 0.3% and Ulta down 18.0%.

Compiling that data together, here’s how ATG and WoW spend growth changed for cosmetics spending last week:

Weekly spend growth: -13.3%

Average ticket growth: 1.2%

TikTok Shop Spending

Showing similar positive growth as last week, TikTok Shop spending continued to increase this week, with:

Weekly spend growth: 14.7%

Average ticket growth: 0.3%

This consistent week-over-week growth seems to suggest that more consumers are relying on this newer e-commerce option for this year’s holiday shopping.

Other Retail Categories

With across-the-board positive growth in ATG and mixed WoW spend growth, retail spending had some clear “winners” this week — namely, Wholesale Clubs and Discount Stores.

That’s because ATG for Wholesale Clubs and Discount Stores was up 24.8% and 13.7%, respectively, while weekly spend growth for these sectors increased by 15.1% and 1.2%, respectively.

Here’s how weekly spend growth evolved this week across various other retail categories:

Grocery spend growth: -8.1%

Wholesale Club spend growth: 15.1%

Discount Store spend growth: 1.2%

Hardware & Home Supply growth: -7.7%

Key Takeaways & Comparisons

Contextualizing this week’s retail transaction data with recent consumer intelligence, some deeper insights begin to come to light, including:

General Retail Momentum: The 9.6% growth in General Retail, led by Amazon's 15.8% increase, suggests continued strong holiday shopping activity following the Black Friday surge. Higher average ticket sizes indicate consumers are making substantial purchases.

Fast Fashion Correction: The -11.0% decline in Fast Fashion, with significant drops at major retailers (ZARA -29.9%, H&M -33.0%), likely reflects a natural pullback after the aggressive Black Friday promotions.

Cosmetics Mixed Performance: Despite increased average ticket sizes, both Sephora (0.3%) and Ulta (-18.0%) saw moderated spending, suggesting a cooling off after strong Black Friday beauty purchases.

Wholesale Club Strength: A notable 15.1% growth with a 24.8% increase in average ticket size indicates consumers are making larger bulk purchases, possibly stocking up for holiday gatherings.

TikTok Shop Consistency: Maintained positive momentum with 14.7% growth, showing sustained engagement on the platform during the holiday season.

The data this week presents a nuanced picture of post-Black Friday shopping behavior. While some categories show expected declines after major promotions, others demonstrate continued strength, suggesting consumers are spreading their holiday purchases across the season. Specifically:

The significant increase in average ticket sizes across multiple categories (General Retail 7.8%, Wholesale Club 24.8%, Discount Store 13.7%) indicates that while transaction volumes might be lower, consumers are making larger purchases when they do shop.

The decline in Grocery (-8.1%) and Hardware & Home Supply (-7.7%) spending might reflect a shift in consumer focus toward gift purchases rather than household essentials or home improvements during this period.

As we move deeper into December, we'll be watching to see how these spending patterns evolve through the remainder of the holiday shopping season, particularly as we approach last-minute shopping periods.

Remember, Facteus analyzes over $3.1 trillion in consumer spending from more than 120 million individual consumers, providing comprehensive insights across various industries.

If you have any questions or would like to explore how Facteus' data can support your business decisions, please don't hesitate to reach out.

Best regards,

Explore Our Win the Week™ Retail Spending Series