In November 2025, Starbucks created two very different exclusive offerings within the same two-week window. One drove $64 million in incremental revenue and created a cultural phenomenon. The other – a Frozen Peppermint Hot Chocolate available only at Target-based Starbucks locations – seems like it may have a different fate. The contrast between these two strategies offers a masterclass in what drives real consumer demand vs. what looks good on paper.

The Bearista Phenomenon: When Exclusivity Creates Real Value

On November 6, 2025, Starbucks released a $29.95 glass cold cup shaped like a teddy bear wearing a green beanie. Within hours, the Bearista cup had sold out nationwide, triggered overnight queues, sparked physical altercations in stores, and created a resale market with listings reaching $1,400 on eBay. Police were called to break up fights. Competitors like Walmart and ALDI rushed to create knockoff versions within 48 hours.

But was the exclusive offer just a viral frenzy, or did it have a real-life impact on sales? Transaction data reveals the Bearista launch wasn’t just social media noise – it translated into substantial, sustained sales growth.

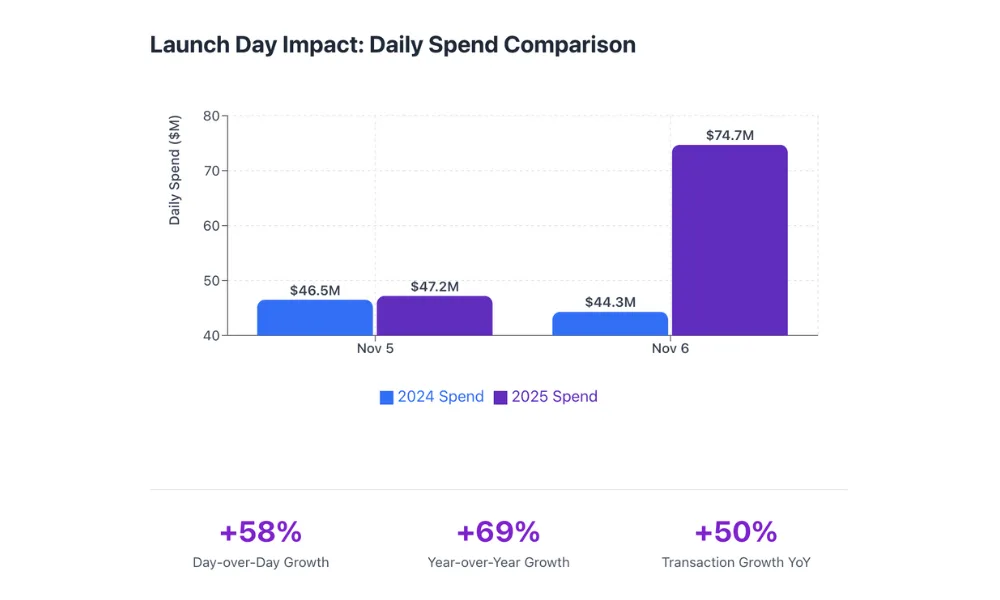

Launch Day Impact (November 6, 2025):

- Transactions jumped 36.5% compared to the previous day

- Average order value increased 15.9%

- Total daily spend reached $74.7 million, up 58.2% from $47.2 million the day before

- Year-over-year, transactions were up 50.4% and spend increased 68.5%

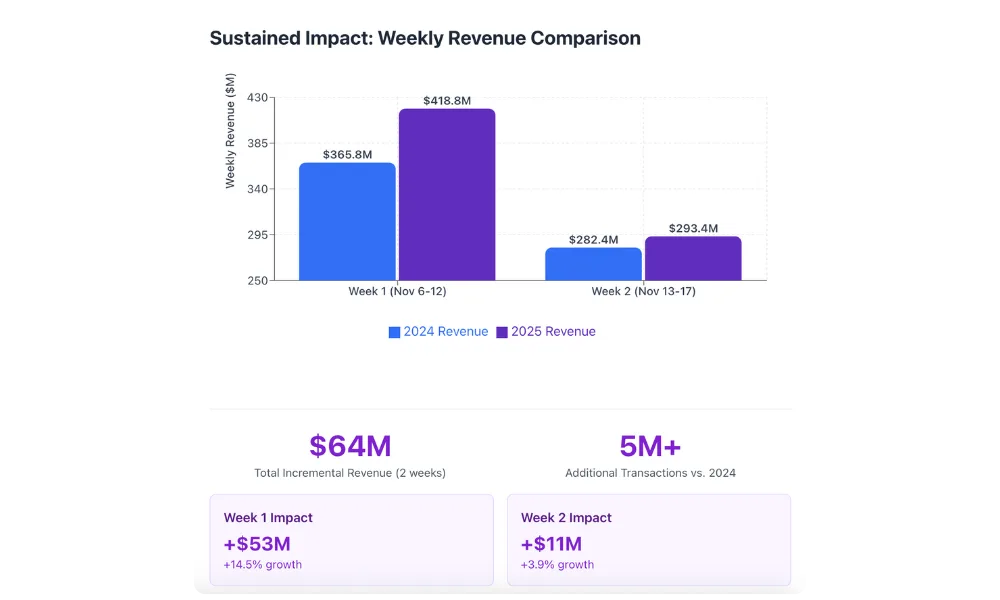

Two-Week Cumulative Results (November 6-17, 2025):

- 5 million additional transactions compared to the same period in 2024 (+11.5%)

- $64 million in incremental revenue over two weeks (+9.9% YoY)

- The first week post-launch generated $53 million in additional spend

- Even the second week maintained elevated performance with $11 million in incremental revenue

- Five days exceeded 4 million transactions in 2025 versus only one day in the comparable 2024 period

This wasn’t a one-day spike that immediately returned to baseline. The data shows sustained elevation in both traffic and spending that extended well beyond the launch date. The week following the Bearista release averaged 16.3% higher daily transactions than the prior week and maintained 16.7% growth year-over-year.

Why the Bearista Cup Worked: The Four Pillars of Demand Creation

The Bearista success rested on four fundamental elements that distinguished it from typical promotional merchandise:

1. Genuine Product Desirability

The Bearista cup succeeded because people actually wanted it, independent of its Starbucks association. The design hit multiple psychological and aesthetic triggers: it was undeniably cute, highly photogenic for social media, and evoked nostalgia through its teddy bear shape. As retail analyst Neil Saunders noted in interviews following the launch, the product created “instant joy” that resonated emotionally with consumers.

The cup’s three-dimensional bear design made it unique in Starbucks’ merchandise history. Unlike flat graphics on standard tumblers, the sculptural quality gave it legitimate collectible value. Customers weren’t just buying branded merchandise – they were acquiring what felt like a limited-edition art collectible that happened to hold beverages.

2. Social Currency and Virality

The Bearista cup became a status symbol almost immediately. Obtaining one signaled being “in the know,” arriving early enough, or being dedicated enough to wait in line. Social media exploded with posts from successful hunters displaying their prizes, which only intensified FOMO (fear of missing out) among those who missed out.

Research from Eventbrite indicates nearly 70% of millennials experience FOMO regularly, making scarcity-driven releases particularly effective with younger consumers. The Bearista capitalized on this psychology perfectly. Each Instagram post of someone with the cup served as both celebration and provocation, driving more people to stores.

The virality extended beyond Starbucks’ control in productive ways. When competitors like Walmart launched $14 knockoffs and ALDI posted cheeky commentary (“That Seattle-based coffee chain could neva”), they amplified the cultural conversation around the product without diluting its perceived value. If anything, the imitations validated that Starbucks had created something genuinely desirable rather than just another piece of branded merchandise.

3. True Scarcity (Not Artificial Limitation)

While Starbucks faced criticism for inadequate inventory – with some stores receiving as few as one or two cups – the scarcity appears to have been genuine miscalculation rather than manufactured hype. A Starbucks spokesperson stated the company “shipped more Bearista cups to coffeehouses than almost any other merchandise item this holiday season” but demand “exceeded even our biggest expectations.”

This distinction matters. Consumers can sense the difference between artificial scarcity used as a marketing tactic and genuine supply constraints from unexpected demand. The Bearista situation felt authentic – stores weren’t holding back inventory, resellers weren’t primary channels, and Starbucks issued apologies rather than celebrating the sellout. This authenticity, in some ways, made the product even more desirable.

The in-store-only availability also created urgency that online sales never could. Digital scarcity often feels abstract; physical scarcity with visible line-ups and empty shelves triggers more immediate psychological responses. Customers could see with their own eyes that the product was genuinely limited, driving faster decision-making and higher willingness to wait or return multiple times.

4. Cultural Timing and Holiday Context

The Bearista launched at the beginning of Starbucks’ holiday season, when consumer sentiment is already primed for seasonal purchases and gift-giving. The product served multiple purposes: personal treat, potential gift, and social media content. This multi-functionality expanded its addressable market beyond just Starbucks collectors to general gift-shoppers and holiday enthusiasts.

The timing also capitalized on the collectibles market boom. The global collectibles market reached $412 billion in 2024, demonstrating consumers’ willingness to pay premium prices for exclusive items. The Bearista positioned itself at the intersection of functional merchandise and collectible novelty, appealing to both practical users and collectors.

The Target Collaboration: A Different Kind of ‘Exclusive’

Against this backdrop of proven demand creation, Starbucks announced a partnership with Target: a Frozen Peppermint Hot Chocolate available exclusively at Starbucks cafés inside Target stores, starting November 18, 2025. Priced at $5.95 for a grande, the Frappuccino-based drink represents the “first-ever holiday drink collaboration” between the two companies.

Both companies need wins. Target faces two consecutive quarters of declining foot traffic, partly from DEI policy backlash, and has lost over a third of its stock value this year. Starbucks continues its challenging turnaround under CEO Brian Niccol, closing stores, conducting layoffs, and facing ongoing union strikes. As CNN reported, these are “two of America’s most embattled retail chains” hoping to “drum up some excitement from customers this holiday season.”

The strategy is transparent: use beverage exclusivity to drive Target foot traffic during critical holiday shopping weeks. Target positions the drink as “the perfect companion for holiday shopping runs,” suggesting they hope customers will combine Starbucks visits with retail browsing.

Why the Target Collaboration Will Likely Fall Short

While the Bearista cup demonstrated what drives real consumer demand, the Target collaboration appears to lack several critical elements that made the Bearista successful:

1. Limited Product Desirability

A Frozen Peppermint Hot Chocolate, while potentially tasty, lacks inherent distinction. Peppermint beverages are ubiquitous during the holiday season – available at countless coffee shops, restaurants, and even in home preparation. The flavor combination isn’t novel or surprising. Unlike the Bearista’s unique visual design, this is essentially a seasonal flavor variation indistinguishable from competitors once consumed.

The drink also lacks “Instagram-ability.” The Bearista cup created lasting social currency – owners could photograph it, post it on social media, and use it throughout the season. A beverage, no matter how exclusive in distribution, provides only momentary content value. Once consumed, the social currency disappears.

2. No Meaningful Scarcity

The drink is available at approximately 2,000 Target locations. While technically “exclusive” to Target-based Starbucks, this distribution model creates false scarcity. Most consumers have multiple Target stores within reasonable driving distance, and the product will be available for an extended period rather than selling out in hours.

True scarcity requires either extremely limited supply or extremely limited time. The Target collaboration offers neither. Customers who want the drink will likely be able to obtain it with minimal effort, eliminating the urgency that drove Bearista success. There’s no racing to stores at dawn, no competing with other customers, no fear of missing out.

3. Wrong Customer Journey

The Bearista cup aligned with natural consumer behavior: people already visit Starbucks for beverages, so adding a merchandise purchase is a logical extension of that trip. The Target collaboration inverts this logic, asking customers to make a special trip to Target specifically for a beverage they could approximate at numerous other locations.

Target customers shopping for household goods, clothing, or groceries may incidentally visit the in-store Starbucks, but the exclusive drink is unlikely to drive incremental destination trips. As retail analyst Neil Saunders told CNN, the drink might “nudge people into visiting Target just to try the drink,” but he doesn’t expect it to “move the foot-traffic dial in a major way.”

4. Distribution Play vs. Demand Creation

Fundamentally, the Target collaboration is a distribution strategy disguised as demand creation. It assumes existing Starbucks beverage demand and attempts to redirect it to Target locations. This approach doesn’t create new desire; it merely shifts where existing desire is fulfilled.

The Bearista, conversely, created entirely new demand. People who had never purchased Starbucks merchandise suddenly wanted this specific product – and they wanted it bad enough to fight for it. The collaboration drink will likely attract existing Starbucks consumers who happen to be near Target but won’t generate new customer segments or fundamentally change purchase behavior.

5. Partnership Dilution

When two struggling brands collaborate, the partnership often signals weakness rather than strength. Instead of each brand bringing unique strengths to create something greater than the sum of parts, this collaboration reads as two declining retailers hoping the other’s customer base will save them.

Target’s recent struggles stem partly from broader retail challenges and partly from self-inflicted wounds around diversity policies. Starbucks faces union conflicts, store closures, and perceptions of declining value. A joint promotion doesn’t address either company’s fundamental challenges – it just shares the same declining customer base.

The Broader Lesson: Demand Creation vs. Tactical Desperation

The contrast between these two strategies illustrates a fundamental principle in retail: exclusivity alone doesn’t drive demand. True demand creation requires products or experiences consumers genuinely want, presented in ways that create urgency and cultural relevance.

The Bearista cup succeeded because it was:

- Genuinely desirable (cute, photogenic, collectible)

- Socially valuable (status symbol, content creation)

- Authentically scarce (unexpectedly high demand)

- Culturally timed (start of holiday season)

The Target collaboration lacks most of these elements:

- Limited desirability (commodity seasonal flavor)

- Minimal social value (temporary beverage, not content-worthy)

- False scarcity (widely available, extended timeframe)

- Questionable timing (two struggling brands joining forces)

Starbucks generated more revenue in two weeks from the Bearista phenomenon than the Target collaboration will likely generate in its entire run. The cup drove a 50.4% increase in transactions on launch day alone, sustained double-digit percentage growth for weeks afterward, and created cultural moments that earned media far beyond Starbucks’ marketing spend.

What Target and Starbucks Should Have Done Instead

If the goal was driving Target foot traffic through Starbucks exclusivity, a more effective approach would have mirrored Bearista’s success factors:

Create merchandise exclusivity, not beverage exclusivity. Target-based Starbucks locations could have offered exclusive, highly designed holiday merchandise available only at Target stores. Make it collectible, Instagram-worthy, and limited in quantity. A special edition tumbler or ornament would create a destination appeal.

Manufacture genuine scarcity. Rather than distributing across 2,000 locations indefinitely, release limited quantities at specific intervals. Create appointment shopping moments: “100 cups available at each Target on November 20, first-come first-served.” This builds urgency and an event-like atmosphere.

Leverage Target’s unique assets. Target has relationships with designers and brands that Starbucks doesn’t. A collaboration product from a Target-exclusive designer brand (like a tumbler designed by Hearth & Hand with Magnolia or a capsule collection with another Target partner) would leverage distinctive capabilities neither brand alone possesses.

Create social sharing incentives. The Bearista cup inherently encouraged sharing because it was so photogenic. The Target collaboration could have included shareable elements: special holiday cups with unique designs available only at Target, or social media-worthy presentation that encourages posting and tagging.

Will the Target Collaboration Fail Completely?

Probably not. The drink will likely generate some incremental foot traffic, particularly from Starbucks loyalty members who receive early access and might already be Target customers. Some customers shopping at Target will try the drink opportunistically. The collaboration will likely produce modest sales, generate some local news coverage, and perhaps marginally improve November and December metrics for both companies.

But it won’t create cultural moments. It won’t drive the urgency, excitement, or social conversation that the Bearista cup generated. It won’t produce overnight lines, resale markets, or competitor knockoffs. Most importantly, it won’t demonstrate the kind of demand creation that changes business trajectories for struggling retailers.

As Saunders concluded in his CNN interview, “Every little bit helps – especially since Target needs it.” That’s the problem: when strategies are justified by “every little bit helps,” they’re unlikely to deliver transformational results.

The Bottom Line

Exclusive offerings can drive significant business results, but only when they create genuine demand rather than simply redistributing existing demand. The Bearista cup proved that products with real desirability, authentic scarcity, social currency, and cultural timing can generate tens of millions in incremental revenue and sustained traffic increases.

The Target collaboration, while a logical partnership on paper, lacks most of these critical elements. It’s a distribution play during a period when both companies need demand creation. It’s a tactical response when strategic transformation is required.

The data from the Bearista launch is unambiguous: when Starbucks creates something people truly want, they’ll wait in line at dawn, drive to multiple locations, and pay premium prices. The question isn’t whether exclusivity works – it’s whether the exclusive offering is actually worth the effort.

A seasonal beverage flavor available at 2,000 locations probably isn’t. A collectible bear cup with inherent desirability definitely was.

Whether the Target partnership will deliver even modest returns remains to be seen, but the contrast with the Bearista phenomenon suggests that partnerships born from mutual weakness rarely create the kind of demand that transforms struggling businesses. Sometimes what looks like strategic collaboration is actually two companies hoping the other will solve problems neither can fix alone.

Methodology

This analysis is based on real-world credit and debit card transaction data from Facteus for Starbucks locations nationwide. Data analyzed includes transaction volume, average order value (AOV), and spend data covering the period from October 2024 through November 2025. The dataset includes daily metrics, allowing for day-over-day, week-over-week, and year-over-year comparisons.

Key metrics examined include:

- Transaction volume: Total number of customer transactions per day

- Average order value (AOV): Average spend per transaction

- Total spend: Aggregate daily revenue

All financial figures represent year-over-year growth percentages and absolute dollar increases. Social media insights, resale market data, and industry analyst commentary were sourced from news coverage and marketing analysis published between November 6-18, 2025.

Disclaimer: This analysis provides a high-level view based on aggregated transaction data. While the insights are meaningful, this represents a preliminary examination and should be considered alongside other market factors and business context.

Want to learn more about Facteus data? Schedule a demo with our team!