Skip to content

Skip to content

The holiday shopping season doesn’t start on Black Friday anymore – and it certainly doesn’t end there. With promotions now launching weeks before Thanksgiving, consumers are spreading out their purchases more intentionally than ever. So, let’s talk about what, where, and when they’re likely to spend.

At Facteus, we analyze billions of daily credit and debit card transactions, giving us a near real-time view of how Americans behave across retailers, categories, and channels. And heading into the Cyber Five (Thanksgiving through Cyber Monday), the data is already starting to paint a clear picture.

We’ve compiled our top four predictions for this year’s holiday shopping surge. Here’s what the data suggests to expect:

Prediction #1 – Consumers Will Spend Earlier (and More Strategically)

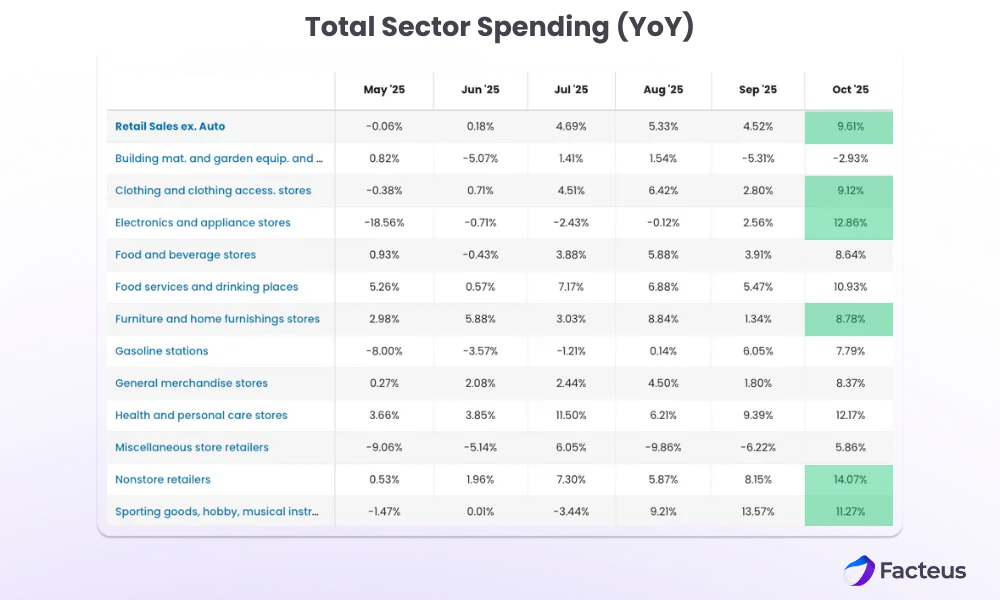

Promotions hit mailboxes and inboxes as early as October – and consumers responded. Spend across major retail categories (excluding auto) was already up 9.61% year-over-year in October as shoppers pulled forward gift buying and big-ticket purchases.

During the 2024 holiday season, consumers spent $186 billion in November alone. This year, retail spend is already well above $120 billion, and that’s before the traditional “kickoff” even begins.

All signs point to a consumer who didn’t wait for Black Friday – they started early and are likely to keep going. A survey from the National Retail Federation (NRF) reports that 58% of holiday shoppers had already begun making holiday purchases by early November.

For retailers, early momentum means one thing: promotional intensity can’t just peak on the big days. It needs to stay consistent throughout the entire season.

Prediction #2 – Big-Ticket Categories Will Drive Outsized Growth

Home goods, electronics, and other high-ticket categories are showing early-season strength, with average order values climbing throughout October and early November.

Facteus sector-level data shows nonstore retailer sales were up 14.1% YoY in October, making online and direct-to-consumer channels the fastest-growing sectors we analyzed.

Other major year-over-year gains include:

- Electronics & Appliances: +12.9%

- Apparel: +9.1%

- Sporting Goods & Hobbies: +11.3%

- Home Furnishing & Furniture: +8.8%

Consumers aren’t just shopping more – they’re buying bigger. With deep discounts expected again this year (electronics hit 31% off on Black Friday 2024, per Adobe), shoppers are likely to pull the trigger on high-consideration purchases they’ve been waiting on.

Categories like appliances, jewelry, and large electronics have already seen early-season spikes, and we expect big-ticket items to fuel record-setting growth throughout the Cyber Five.

Prediction #3 – Value-Seeking Behavior Will Intensify

Inflation may be easing, but the pressure on consumers hasn’t fully lifted. Prices rose just 2.4% YoY as of September 2025 – the smallest increase since early 2021. But the cumulative impact of 21.4% inflation since 2020 remains top of mind for most households.

In Facteus’ transaction data, we’re seeing higher cross-retailer churn – clear evidence that loyalty may be taking a backseat to value. Consumers are switching merchants more readily, driven by price sensitivity and a desire to maximize savings.

Expect shoppers to be both opportunistic and brand-agnostic. According to a recent survey by Mastercard, 58% of U.S. households remain “extremely concerned” about inflation, and nearly 70% say they’re using sales and coupons more often.

This is a season where the deal – not the brand – wins.

Prediction #4 – The Cyber Five Will Set the Tone for December

The first five days of the holiday surge will dictate how retailers behave for the rest of the season. Whether consumers come out strong or hold back, we’ll see immediate downstream effects on:

- Promotional duration: momentum will be either sustained or “panic-discounted”

- Category-level markdowns: underperformers will be cut deeper; overperformers will tighten

- Customer acquisition pushes: early winners will double down; laggards will scramble

- Post-holiday inventory plans: the Cyber Five signals what will move – and what won’t

Mastercard reports that the five days before Christmas accounted for 10% of all 2024 holiday spending, a reminder that late-season urgency remains powerful. December 23rd was once again the season’s top shopping day, showing just how fluid behavior stays right until the finish line.

Our expectation: Cyber Monday will be the highest-spend day of the entire season.

As online shopping continues to accelerate, Cyber Monday has emerged as a true rival to Black Friday – and in recent years, the clear frontrunner. If early transaction momentum holds, 2025 could cement Cyber Monday as the undisputed peak of holiday retail.

The Good News?

Facteus analyzes real-world transaction data from more than 185 million active credit and debit accounts – refreshed daily. That means you can track consumer behavior and competitive shifts as they happen, not weeks later.

If you want to capitalize on early trends this holiday season, you need answers before the moment passes. That’s exactly what our data delivers.